Systematic Investment Plans (SIPs) have become one of the most popular ways to invest in mutual funds. They are simple, disciplined, and effective for long-term wealth creation. But while many investors focus on returns, they often overlook an equally important aspect—taxation.

Understanding how SIPs are taxed can help you plan better, avoid surprises, and maximize your returns. At Growthvine, our experienced financial advisors, financial planners, and financial consultants help investors not only grow their wealth but also make tax-efficient decisions.

What is SIP and How Does It Work?

A SIP (Systematic Investment Plan) allows you to invest a fixed amount regularly (monthly, weekly, etc.) in mutual funds.

Instead of investing a lump sum, SIPs:

- Build discipline

- Reduce market timing risk

- Benefit from compounding

However, each SIP installment is treated as a separate investment for tax purposes. This is where things get interesting.

How SIPs Are Taxed in India

Taxation of SIPs depends on:

- Type of mutual fund (Equity or Debt)

- Holding period of each installment

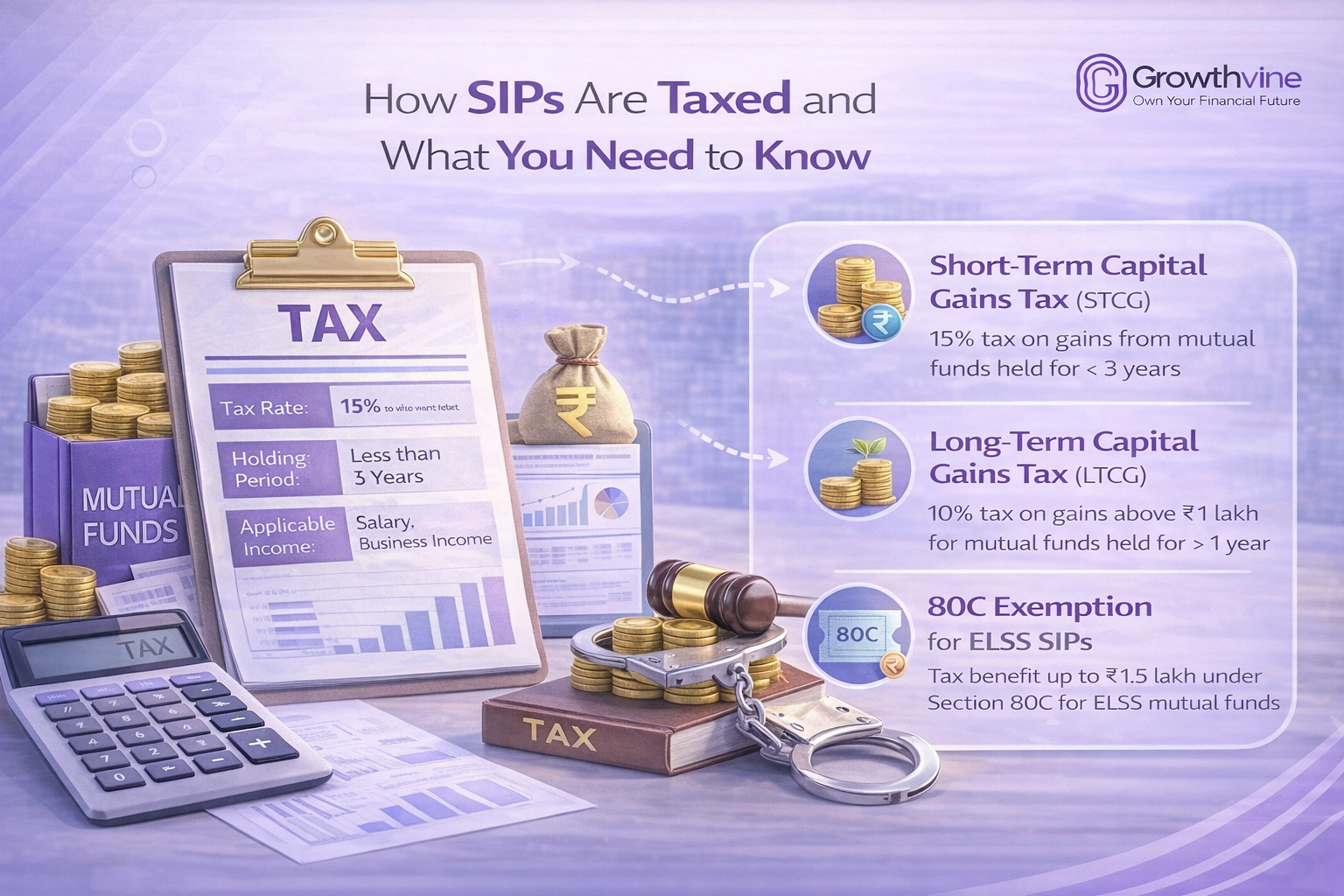

1. Taxation of Equity Mutual Fund SIPs

Equity mutual funds invest primarily in stocks.

Short-Term Capital Gains (STCG)

- Holding period: Less than 12 months

- Tax rate: 15%

Long-Term Capital Gains (LTCG)

- Holding period: More than 12 months

- Tax rate: 10% (only on gains above ₹1 lakh)

Important Note:

Each SIP installment has its own 12-month holding period.

Example:

You invest ₹5,000 monthly via SIP.

- January investment → completes 1 year in next January

- February investment → completes 1 year in next February

If you redeem all units together, each installment will be taxed differently.

A skilled financial advisor can help you plan withdrawals smartly to reduce taxes.

2. Taxation of Debt Mutual Fund SIPs

Debt mutual funds invest in bonds and fixed-income instruments.

Short-Term Capital Gains:

- Holding period: Less than 36 months

- Tax: As per your income tax slab

Long-Term Capital Gains:

- Tax rules depend on prevailing regulations (often slab-based in recent changes)

Debt fund taxation can be more complex, so guidance from a financial consultant is highly recommended.

Why SIP Taxation is Different

Unlike lump sum investments, SIPs involve multiple transactions over time.

This means:

- Each installment is treated separately

- Each has its own purchase date

- Each is taxed individually

This makes tax calculation slightly complex but also offers opportunities for better tax planning.

Key Things You Need to Know About SIP Taxation

1. Every SIP Installment is a New Investment

Each SIP is treated independently for tax purposes.

2. Holding Period Matters

The longer you stay invested, the lower your tax liability (especially in equity funds).

3. Redemption Timing is Crucial

Withdrawing at the right time can reduce taxes significantly.

4. ELSS SIPs Have Lock-in

Equity Linked Saving Schemes (ELSS) have a 3-year lock-in for each SIP installment.

How to Reduce Taxes on SIP Investments

While taxes are unavoidable, you can manage them smartly.

1. Stay Invested for the Long Term

Avoid early withdrawals to benefit from lower tax rates.

2. Plan Systematic Withdrawals

Instead of redeeming everything at once, withdraw strategically.

3. Use Tax-Loss Harvesting

Offset gains with losses to reduce taxable income.

4. Choose Tax-Efficient Funds

Select funds aligned with your financial goals and tax situation.

At Growthvine, our financial planners design strategies that balance returns and tax efficiency.

Common Mistakes Investors Make

Avoid these common SIP taxation mistakes:

- Thinking SIP is tax-free

- Ignoring holding period rules

- Redeeming all units at once

- Not tracking individual installments

- Making emotional investment decisions

A professional financial advisor can help you avoid these pitfalls.

Role of Growthvine in SIP Tax Planning

At Growthvine, we believe that smart investing includes smart tax planning.

Our services include:

- SIP portfolio analysis

- Tax-efficient withdrawal strategies

- Guidance from expert financial consultants

- Personalized financial planning

We help you understand not just how to invest—but how to maximize what you keep.

When Should You Consult a Financial Expert?

You should seek expert help if:

- You have multiple SIPs

- You plan to redeem investments

- You want to reduce tax burden

- You are unsure about tax rules

A qualified financial planner can simplify the process and optimize your investment strategy.

Final Thoughts

SIPs are one of the best tools for long-term wealth creation, but understanding their taxation is essential for maximizing returns.

To summarize:

- Each SIP installment is taxed separately

- Equity and debt funds have different tax rules

- Holding period plays a crucial role

- Smart planning can reduce tax liability

With expert guidance from Growthvine’s team of financial advisors, financial planners, and financial consultants, you can build a tax-efficient investment strategy that works for your goals.

CFA-certified investment advisor with 15+ years of experience at Morgan Stanley, BofA Merrill Lynch, and Fidelity. SEBI-registered advisor (INA000018665).