Planning for retirement is no longer optional — it’s essential. With rising living costs and longer life expectancy, choosing the best retirement plan in India can determine how comfortably you live after your working years. Among the most popular options today is the National Pension System (NPS), which comes in two forms: corporate NPS and individual NPS.

While both aim to build a retirement corpus, they differ in structure, benefits, and suitability. Let’s break down the differences so you can choose wisely and align your savings with the best retirement pension plan for your future with Growthvine.

What is NPS?

The National Pension System is a government-backed retirement savings scheme regulated by the Pension Fund Regulatory and Development Authority (PFRDA). It allows individuals to invest regularly during their working years and receive a pension after retirement.

NPS offers market-linked returns, tax benefits, and flexibility — making it one of the most attractive choices for anyone looking for a reliable retirement plan in India.

What is Individual NPS?

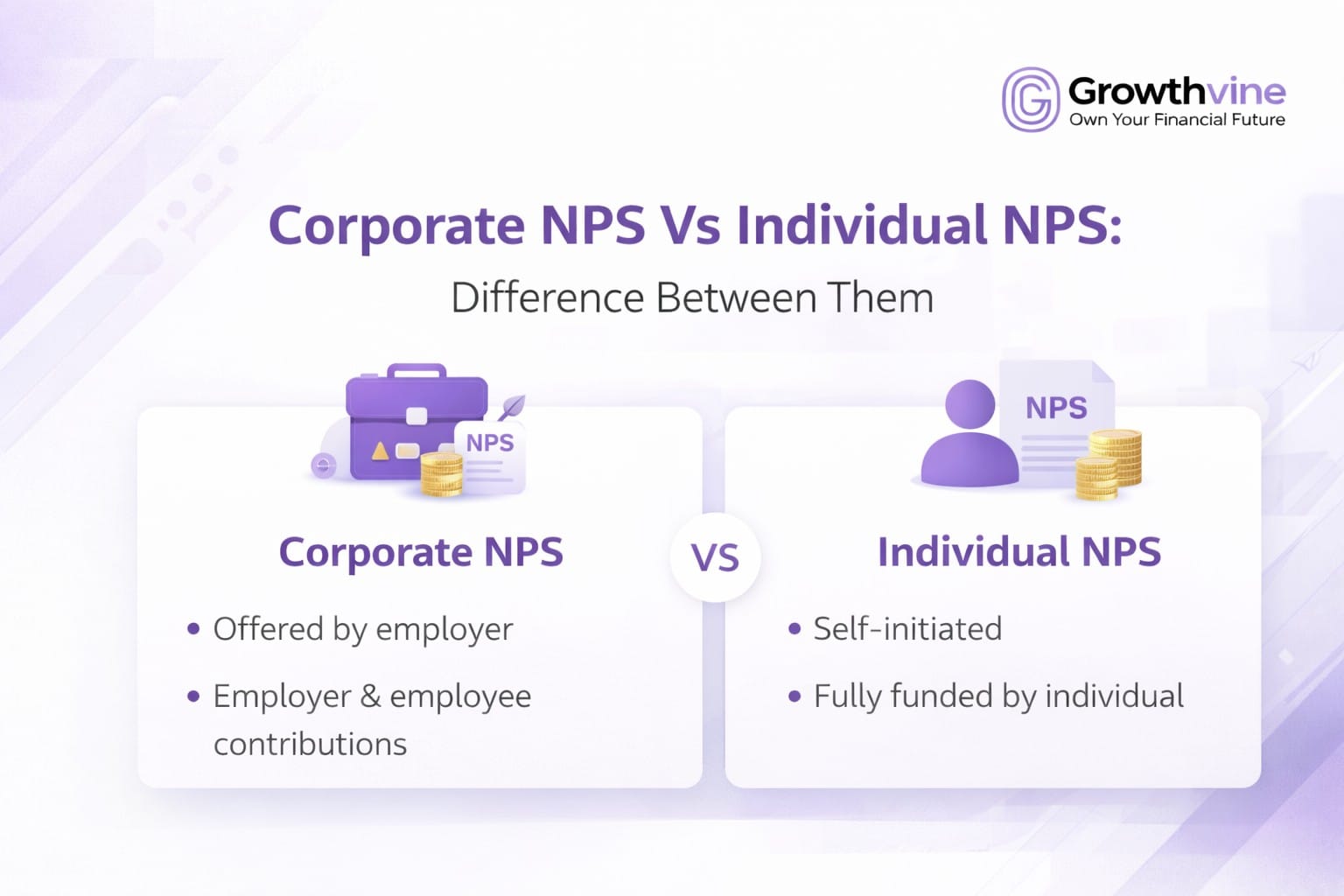

Individual NPS is a voluntary retirement account that any Indian citizen aged 18–70 can open. You can contribute independently, choose your investment mix, and manage the account yourself.

This option works best for:

- Self-employed individuals

- Freelancers

- Professionals without employer retirement benefits

- Anyone wanting to build a personal retirement corpus

Individual NPS gives you full control over contributions and asset allocation. You can invest in equity, corporate bonds, or government securities depending on your risk appetite.

For many people, this flexibility makes it one of the best retirement plans available today.

What is Corporate NPS?

Corporate NPS is offered by employers as part of employee retirement benefits. In this model, the company registers with NPS and contributes to the employee’s pension account alongside the employee’s own contributions.

This structure is ideal for:

- Salaried professionals

- Employees in organized sectors

- Companies wanting to offer structured retirement benefits

Corporate NPS enhances retirement savings by combining employer contributions with tax advantages, making it highly efficient for long-term wealth building.

Financial planners consider it one of the best retirement pension plans for salaried individuals due to its dual contribution structure.

Key Differences Between Corporate NPS and Individual NPS

- Contribution Source

In Individual NPS, only the subscriber contributes.

In Corporate NPS, both employer and employee contribute, boosting retirement savings faster. - Tax Benefits

Both options offer tax deductions under Sections 80C and 80CCD.

However, Corporate NPS provides an additional tax benefit under Section 80CCD(2), where employer contributions are tax-deductible up to specified limits. This makes Corporate NPS more tax-efficient for salaried individuals. - Ease of Investment

Individual NPS requires self-management — you decide how much to invest and when.

Corporate NPS contributions are often automated through payroll, ensuring disciplined savings. - Suitability

Individual NPS suits entrepreneurs, freelancers, and independent workers.

Corporate NPS suits employees in companies offering structured benefits. - Portability

Both accounts are portable across jobs and locations. Even if you change employers, your Corporate NPS account continues seamlessly.

Which One is Better for Retirement Planning?

The answer depends on your employment situation and financial goals.

If you’re self-employed or want full control over investments, Individual NPS may be the better option.

If your employer offers Corporate NPS, it’s usually wise to opt in because employer contributions significantly increase your retirement corpus.

When evaluated purely on tax efficiency and long-term wealth accumulation, Corporate NPS often emerges as the best retirement plan in India for salaried individuals.

How NPS Fits Into Your Overall Retirement Strategy

NPS should ideally form the foundation of your retirement planning. However, relying on a single product may not be enough.

A well-balanced retirement plan may include:

- NPS for long-term pension income

- Mutual funds for growth and liquidity

- Insurance for risk protection

- Fixed income instruments for stability

This combination helps create a diversified strategy that protects you from market volatility while ensuring steady income post-retirement.

Why Professional Guidance Matters

Choosing between Corporate NPS and Individual NPS may seem simple, but optimizing contributions, tax benefits, and asset allocation requires careful planning.

A qualified financial advisor in Delhi Growthvine can help you:

- Select the right pension structure

- Maximize tax savings

- Balance risk and returns

- Build a sustainable retirement income plan

With the right guidance, you can transform NPS from just another investment into a powerful wealth-building tool.

Final Thoughts

Both corporate NPS and individual NPS are strong retirement options backed by government regulation and long-term benefits. The right choice depends on your job structure, income stability, and financial goals.

CFA-certified investment advisor with 15+ years of experience at Morgan Stanley, BofA Merrill Lynch, and Fidelity. SEBI-registered advisor (INA000018665).