When it comes to safe, long-term investments in India, two options often stand out — the Public Provident Fund (PPF) and the Voluntary Provident Fund (VPF). Both are government-backed savings instruments known for stability, tax benefits, and retirement-focused wealth creation. But if you’re planning your investments for 2026, the real question is: which one suits you better?

At Growthvine, we believe that the right investment choice depends on your income structure, financial goals, and tax planning needs. With guidance from a professional investment planner, experienced investment advisor, or registered investment advisor, you can select the option that truly strengthens your financial future.

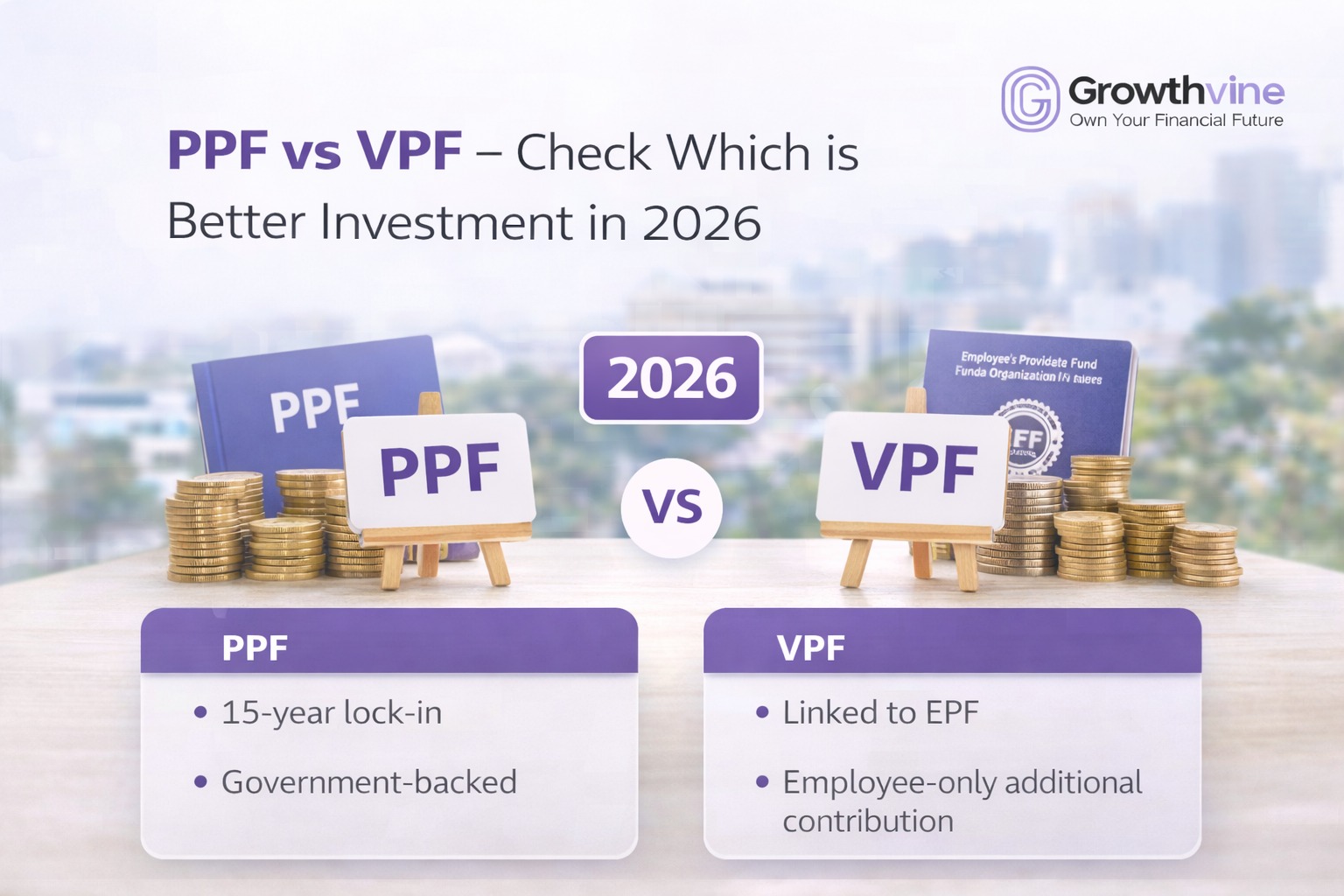

What Is PPF?

The Public Provident Fund (PPF) is a long-term government savings scheme open to all Indian citizens. It is designed to encourage disciplined savings and provide tax-free returns over time.

Key features of PPF include:

- 15-year lock-in period

- Government-declared interest rate (reviewed quarterly)

- Tax benefits under Section 80C

- Completely tax-free maturity amount

- Available through banks and post offices

PPF works well for individuals who want a safe retirement-oriented investment independent of their employer.

Because of its stability and tax-free status, many professionals consult a SIP investment planner to include PPF as the debt component of a diversified portfolio.

What Is VPF?

The Voluntary Provident Fund (VPF) is an extension of the Employee Provident Fund (EPF). It allows salaried employees to voluntarily contribute more than the mandatory 12% of their basic salary to their provident fund account.

Key features of VPF include:

- Same interest rate as EPF (often higher than PPF)

- Contributions deducted directly from salary

- Tax benefits under Section 80C

- Tax-free maturity after continuous service

- Ideal for salaried individuals seeking automatic savings

Since VPF contributions happen through payroll, they encourage disciplined investing. This is why many investment advisors in Delhi and across India recommend VPF for salaried professionals looking to increase retirement savings effortlessly.

PPF vs VPF: Key Differences

- Eligibility

PPF is open to all Indian citizens, including self-employed individuals.

VPF is available only to salaried employees who already contribute to EPF. - Contribution Flexibility

PPF allows annual contributions from ₹500 up to ₹1.5 lakh.

VPF allows contributions beyond the EPF limit, often up to 100% of basic salary and DA. - Interest Rates

VPF usually offers slightly higher returns since it follows EPF rates.

PPF rates are stable but sometimes lower than EPF. - Liquidity

PPF has partial withdrawal options after year 7.

VPF funds are typically locked until retirement or job change, though loans may be available. - Risk Level

Both investments are government-backed and extremely safe, making them attractive for conservative investors.

Choosing between the two often depends on your employment status and savings discipline. A professional investment planner can help determine which option aligns better with your long-term financial strategy.

Which One Is Better in 2026?

The answer depends on your financial profile.

If you are salaried and already contributing to EPF, VPF may be the better choice because:

- It offers higher interest rates historically

- Contributions happen automatically

- It increases retirement savings without extra effort

However, PPF may be better if:

- You are self-employed or run a business

- You want independent retirement savings

- You prefer flexible contributions

- You want a separate tax-free corpus outside employer-linked funds

At Growthvine, our registered investment advisors often recommend using both instruments strategically. VPF can act as your primary retirement savings tool, while PPF can provide diversification and additional tax-efficient income.

How PPF and VPF Fit Into a Modern Investment Plan

In 2026, financial planning is not about choosing one instrument but creating a balanced strategy.

A strong portfolio may include:

- Equity mutual funds through SIPs for growth

- PPF or VPF for stable, long-term savings

- Emergency funds for liquidity

- Insurance for protection

A skilled SIP investment planner or experienced investment advisor Growthvine in Delhi can help combine these components into a portfolio that balances growth, safety, and tax efficiency.

Why Professional Guidance Matters

While both PPF and VPF are simple products, choosing the right contribution levels and integrating them into your broader investment plan requires expertise.

At Growthvine, our team of certified professionals helps investors:

- Evaluate salary structure and tax position

- Optimize retirement savings contributions

- Balance equity and debt investments

- Plan withdrawals strategically

- Build long-term financial security

Working with a registered investment advisor ensures your decisions are not based on trends but on your personal goals and financial reality.

Final Thoughts

Both PPF and VPF remain among the safest investment options available in India in 2026. The better choice depends on your employment type, income stability, and retirement planning goals.

If you are salaried, VPF often offers better returns and disciplined savings. If you want flexibility and independence, PPF remains a powerful long-term investment.

The smartest approach, however, is not choosing blindly but planning strategically. With expert support from Growthvine’s investment planners, trusted investment advisors, and experienced financial professionals, you can turn simple savings instruments into a strong foundation for lifelong wealth.

Because the best investment decision isn’t just about returns — it’s about building a future where your money works for you with confidence and clarity.